SUMMARY

In a simple way it develops in the form of a table, the calculation of the variable cost of a lid, starting from the consumptions necessary for its manufacture.

INTRODUCTION

A fundamental fact, which should be known by the container manufacturer, is the cost of the products produced in their facilities. We dedicate this work to the explanation of how to calculate, in a simple way, the cost of a conventional lid or fund. In other articles, the same calculation will be detailed, in the case of a complete package.

This cost called standard, or also variable or direct cost, includes the evaluation of the direct components, which intervene in the specific production of this element. Then you have to take into account other addends, which must be added to it, to have the full cost. Later we will enter into the definition of them.

CALCULATION OF PREVIOUS DATA

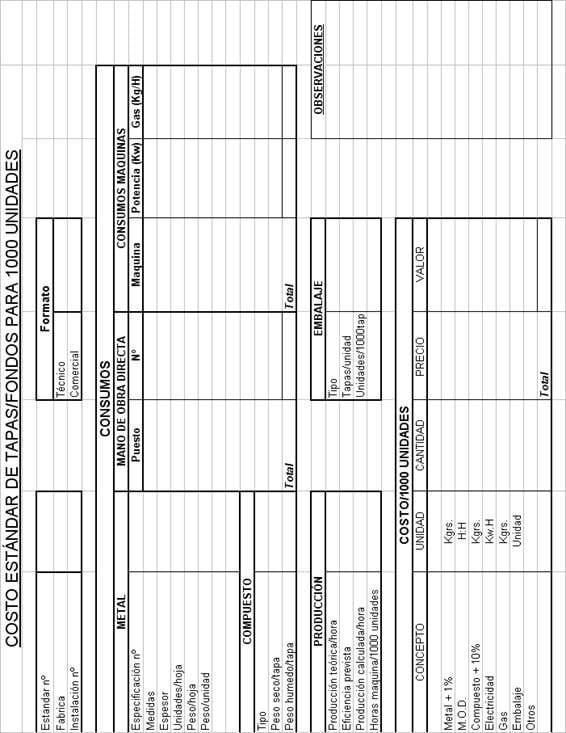

At the end of this writing, figure 1 shows a summary, which summarizes all the operations to follow to perform this calculation. We will discuss the different parameters of it. The execution initially involves filling in the boxes of the table with a series of basic data, then perform with them a few operations that will lead us to the cost.

The calculation is made for a thousand units, since the unit cost is usually very small, and also the quantities of caps / funds that are handled in the industry, are usually always multiples of a thousand.

1º.- In a first box, three data appear:

– Standard nº : Is an order number to identify the cost

– Fabrica : In the case that it is a company with several work centers, it will indicate in what factory the activity is carried out.

– Installation nº : The production lines are usually designated with a code (number or letter). The corresponding to the cover object of the calculation will be indicated.

2º.- In the following box the designations of the calculated Format are reflected

– Technique : Indicates its measurements, for example “caps diameter 73”.

– Commercial : Reflects its use, for example “lids for 1 / 2Kg container”.

3º.- We enter the Consumption chapter, which provides data on the different expenses, which we will have to fill out in this part of the report, such as:

- A) Metal:

– Specification No .: Refers to the internal code of the metal specification sheet.

– Measurements : The dimensions of the sheet used in millimeters will be indicated.

– Thickness : Thickness of the sheet in mm.

– Units / sheet : Quantity of caps that are obtained per sheet.

– Weight / sheet : Expressed in grams.

– Weight / Unit : Result of dividing the Weight / sheet between Units / sheet. It is expressed in grs.

- B) Compound:

– Type : Indicate class, manufacturer and reference. For example: “Water Base Grace OP 770”.

– Dry weight / lid : Specification defined for the type of lid expressed in grams.

– Wet weight / lid : Equal to the dry weight divided by the% solids that the compound has in liquid state.

- C) Direct labor :

– In the Post column the different jobs in the installation will be related: For example: mechanical, press, packer, etc.

– In column No. , the number of people who perform this task will be reflected. When the position is shared with other facilities, the fraction of it used in this line will be indicated. In general, you must flee from shared positions, because if one of the facilities is stopped, it is a bad use of the operator. It is better to create units, independent of each other, with one or more operators, trained in different functions, with a good workload each. Direct labor will be totaled at the end of this column.

- D) Machine consumptions

– Machine : A list of the machines that make up the installation will be made: Scroll, Union, Press, Rizadora, Engomadora, etc.

– Electric power : The installed power in Kw of each machine will be noted in each box. It can be determined by consulting your manual.

– Gas : If the same is used, for example in the oven of the gumming machine, its consumption will also be noted in the box corresponding to the machine in question. The quantity consumed is also usually provided by the equipment manufacturer.

4º.- We now determine the real time for the Production of 1000 caps / funds.

– Theoretical production / hour : It will be defined by the theoretical production speed of the installation, which in turn will be limited by the slowest machine in the line.

– Expected efficiency : It is the real yield in% that the installation obtains, determined by comparison of the real production and the theoretical production during a long period of production.

– Calculated production / hour : Obtained by the product of the theoretical Production and the expected Efficiency.

– Machine hours / 1000 units : Determined from the calculated Production / hour.

5th.- Packaging .

– Type : The means used will be indicated: Plastic bag, paper bag, cardboard boxes, etc.

– Tapas / unit : It must reflect the quantity of lids that fit in each unit of packaging.

– Unit / 1000 covers : No. of packages consumed per 1000 items.

CALCULATION OF STANDARD COST

We enter the final part of the calculation, in it we will make use of the data obtained so far. We repeat that the determination is made for a thousand units. In the lower box we will fill in the second column the consumed quantities of each component first, in the third its price and in the fourth the product of both, which once added will give us the final value of the cost.

The only one that deserves to be discussed is the second one.

– Metal + 1%: Metal consumption (tinplate, TFS, aluminum) per 1000 units. It is the product of the data “Weight / Unit” per 1000, increased by 1% that absorbs the losses due to waste.

– MOD : Number of people x Machine hours / 1000 units.

– Compound + 10%: Wet weight / lid X 1000 with an increase of 10% for losses.

– Electricity : Electricity expenditure. Product of the installed Power in Kw X Hours machine / 1000 units

– Gas : Gas consumption = Gas (Kgrs / H) X Machine hours / 1000 units

– Packaging = Packaging / 1000 units

– Others: It will be indicated if the lid bears any other element, such as neck, handle, etc. reflecting its cost, including its placement. It will have been necessary to have previously calculated the standard cost of this element.

The cost obtained logically does not represent the total cost of the cap. To arrive at the full cost of it, it would be necessary to incorporate a series of fixed costs, such as:

A)

– Repair and Maintenance

– QA

– Warehouses

– Indirect labor

– Spare parts

– Etc.

That is to say, what is understood as Fixed General Expenses of the factory.

B) Financial expenses

C) Commercial expenses

D) Amortizations

E) Licenses and royalty

F) Other

All of them must be previously known and added as a percentage.

Really for the tapas these expenses are not usually added, unless they are sold independently of the container. The normal thing is that they are part of the container and therefore, it would be necessary to calculate the standard cost of the container with its two built-in covers and to add these complements to it. This will be the subject of another work.

Figure nº 1

Theoretical calculation of the volume of rubber required for the closure of a metal container.

Theoretical calculation of the volume of rubber required for the closure of a metal container.

total cost of a soft drink can production line

Supply of packaging and ends

total cost of a soft drink can production line

Supply of packaging and ends

STANDARD CALCULATION COST FROM A CANS “THREE PIECES”

STANDARD CALCULATION COST FROM A CANS “THREE PIECES”

CALCULATION OF THE TABS OF MADE A FLANGE

CALCULATION OF THE TABS OF MADE A FLANGE

SPECIFICATION OF TIN FOR CONTAINER BODIES “3 PIECES “

SPECIFICATION OF TIN FOR CONTAINER BODIES “3 PIECES “

PRODUCT DATASHEET: SAUSED PACKAGING

PRODUCT DATASHEET: SAUSED PACKAGING

PRODUCT TECHNICAL DATA SHEET: ENDS

PRODUCT TECHNICAL DATA SHEET: ENDS

SPECIFICATION OF TIN FOR ENDS

Quotation for the manufacture of metal containers with screw caps

SPECIFICATION OF TIN FOR ENDS

Quotation for the manufacture of metal containers with screw caps

0 Comments